TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

.webp)

A chargeback is more than a refund. It's a reversal forced by the customer's bank, complete with fees, lost product, and a hit to your standing with card networks. Let too many pile up and you risk higher costs or even losing your ability to process cards. The good news: most chargebacks are preventable. This guide walks through exactly how to reduce chargebacks, from understanding why they happen to building a repeatable process that keeps your dispute rate low and protects your revenue.

What is a chargeback?

A chargeback is a transaction reversal initiated when a cardholder disputes a charge with their issuing bank, rather than requesting a refund directly from the merchant. The bank pulls the funds back from your account, notifies you of the dispute, and gives you a window to respond.

Chargebacks exist to protect consumers from fraud and errors, and that protection is enshrined in law. In the United States, the Fair Credit Billing Act gives cardholders the right to dispute billing errors and unauthorized charges, which is the legal backbone of the modern dispute system. The problem is that the same process is frequently misused for purchases customers simply forgot about, regretted, or want refunded without returning the item. Telling legitimate disputes apart from this kind of abuse is the foundation of effective chargeback management.

Chargeback vs. refund: what's the difference?

A refund is something you control. The customer contacts you, you agree, and you return their money directly, usually keeping the relationship intact and avoiding extra fees. A chargeback removes you from the decision entirely. The customer goes to their bank instead of to you, the bank reverses the funds, and you are charged a dispute fee on top of losing the sale. Steering customers toward refunds and easy support is one of the simplest ways to prevent chargebacks before they ever reach the bank.

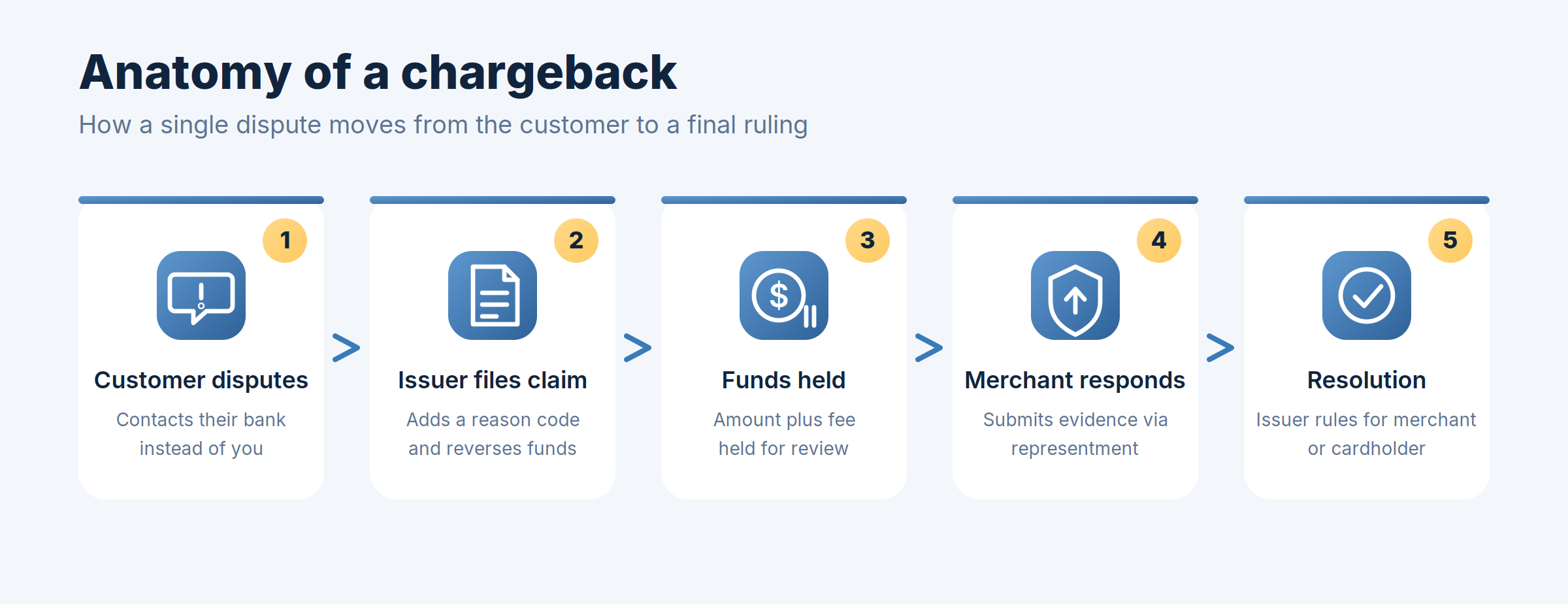

How the chargeback process works

Understanding the lifecycle helps you intervene at the right moments.

It starts when a customer disputes a charge with their bank. The issuer files the claim with a reason code, which is a standardized label describing why the cardholder is disputing, and reverses the funds, pulling the amount plus a fee from you pending review. You then have a fixed window to respond with evidence and fight invalid disputes through a process called representment. The issuer reviews what you submit and ultimately rules for either the merchant or the cardholder. If the dispute escalates, it can move into arbitration handled by the card network, where the losing side pays additional fees.

Knowing this flow is the first step toward dispute prevention, because each stage gives you a chance to act. The U.S. Federal Trade Commission also publishes guidance on consumer payment rights that shapes how banks evaluate these disputes, and reading it from the customer's perspective helps you anticipate the arguments you will need to counter.

Common chargeback reason codes

Every dispute arrives with a reason code from the relevant card network, and the code tells you what kind of evidence you need. While each network maintains its own system, most codes fall into four broad buckets:

- Fraud: the cardholder claims they did not authorize the transaction. These are the most common and often the hardest to fight.

- Authorization: the transaction was processed without proper approval, or after a card was declined or expired.

- Processing errors: duplicate charges, incorrect amounts, or currency mistakes.

- Consumer disputes: the product never arrived, arrived damaged, was not as described, or a promised refund was never issued.

Mapping your incoming disputes to these categories shows you where your real problems are. A spike in "product not as described" points to your listings or shipping; a spike in fraud codes points to weak screening at checkout.

Why chargebacks hurt more than you think

Each chargeback costs you the sale, the product, and a fee, often $15 to $100 per dispute. But the direct cost is only part of the story.

Card networks track your chargeback ratio, the percentage of your transactions that turn into disputes, and they enforce hard thresholds. Visa runs its Dispute Monitoring Program and Mastercard runs the Excessive Chargeback Program; cross their limits and you can be placed in costly monitoring, hit with per-dispute fines, or have your account terminated outright. You can read more about how each network frames merchant responsibilities directly on the Visa and Mastercard sites.

For businesses already flagged as elevated risk, the stakes climb even higher, which is why disciplined dispute control sits at the center of managing high-risk merchant accounts. A rising ratio can also make it harder and more expensive to keep reliable payment processing in place, since acquirers price risk into your rates.

The three root causes of chargebacks

Almost every dispute traces back to one of three sources, and the cure is different for each.

- True fraud: a stolen card or stolen card details are used without the real cardholder's knowledge. The defense here is strong upfront screening and authentication.

- Friendly fraud: a genuine customer disputes a charge they actually made, whether by mistake or on purpose. The defense is clear records, recognizable billing, and easy refunds that remove the incentive to dispute.

- Merchant error: unclear descriptors, double billing, slow shipping, or confusing policies push otherwise happy customers to their bank. The defense is fixing your own operations.

Diagnosing which cause dominates your disputes tells you where to spend your effort. Most merchants are surprised to find that friendly fraud and merchant error, not true fraud, drive the majority of their volume.

How to prevent chargebacks

Prevention is far cheaper than fighting disputes after the fact. These six tactics stop most chargebacks before they start and keep your chargeback rate low.

Use a clear billing descriptor. The name that appears on a customer's statement should obviously match what they bought. Cryptic descriptors are one of the leading causes of "I don't recognize this charge" disputes, and fixing yours is often the single highest-impact change you can make.

Make refunds easy. An easy refund is almost always cheaper than a chargeback, because it avoids the dispute fee and keeps the customer's trust. A frictionless return policy quietly removes the main reason customers go to their bank in the first place.

Deploy fraud tools and authentication. Turn on Address Verification Service (AVS) and CVV checks, and use 3-D Secure, which adds a verification step that can shift liability for certain fraud disputes away from you. Layer on AI fraud detection to flag risky orders in real time before they ship.

Track delivery on every order. Tracking numbers, signatures, and delivery confirmation are your strongest evidence against "item never arrived" claims, and collecting them by default means the proof is already waiting when a dispute lands.

Be easy to reach. A visible phone number, responsive email, and live chat give frustrated customers somewhere to go that isn't their bank. Many disputes are simply support requests that took the wrong path.

State your policies clearly. Publish transparent refund, shipping, and cancellation terms, and make customers acknowledge them at checkout. Clear policies both reduce confusion and strengthen your evidence if you ever need to contest a dispute.

For card-not-present and online businesses, pairing these habits with strong PCI compliance and secure handling of card data, in line with the PCI Security Standards Council, closes the gaps fraudsters look for.

How to fight invalid chargebacks

When a dispute is illegitimate, you can fight it through representment by submitting compelling evidence to the issuing bank. Strong evidence typically includes receipts and order confirmations, delivery and tracking records, customer communication logs, IP and device data, AVS and CVV match results, and a copy of the terms the customer agreed to.

Three habits decide whether you win. First, respond before the deadline, because late or incomplete responses almost always mean an automatic loss. Second, keep your evidence organized so you can assemble a rebuttal quickly rather than scrambling. Third, be selective: focus your energy on disputes you can realistically win, and don't burn hours fighting cases where the customer clearly has the stronger claim. Winning representment also signals to networks that you actively manage fraud, which matters for your long-term standing.

Build an ongoing chargeback management process

Reducing chargebacks is not a one-time project. The merchants who keep their chargeback rate low treat it as a continuous loop.

Start by monitoring your ratio against network thresholds every month, well before you approach a limit. When disputes come in, categorize them by reason code and root cause so you can spot patterns, then fix the underlying issue, whether that's a confusing product page, a slow fulfillment step, or a descriptor no one recognizes. Consider enrolling in dispute alert and prevention networks, which notify you of a brewing dispute in time to issue a refund and avoid the chargeback entirely. Finally, review your win rate on representment and refine the evidence you submit over time. Done consistently, this loop turns chargebacks from a recurring tax into a managed, shrinking line item.

Free Demo with Chris

Free Demo with Chris

.webp)