TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

If a bank or processor has ever called your business "high-risk," you already know how frustrating the label can feel. It often shows up as a declined application, a frozen payout, or a set of fees that seem to climb with every sale. The good news is that being classified as high-risk does not mean you cannot accept card payments reliably. It simply means you need the right processing partner and the right setup.

This guide walks through everything a business owner needs to understand about high-risk payment processing. You will learn what a high-risk merchant account actually is, why businesses end up in this category, what to expect in terms of fees and reserves, how to choose a processor, and how to get approved and stay approved. Whether you are launching in a flagged industry or you have just been dropped by a generic provider, this is your starting point.

What is a high-risk merchant account?

A high-risk merchant account is a payment processing account designed for businesses that acquiring banks consider more likely to generate chargebacks, fraud, or regulatory complications. The underlying service is identical to a standard merchant account. It lets you accept credit and debit card payments. What changes is the pricing, the underwriting, and the risk controls, all of which are tailored to a higher-risk profile.

It helps to remember that "high-risk" is a label assigned by banks and card networks, not a verdict on how well you run your company. Plenty of profitable, carefully managed businesses fall into this category purely because of the industry they operate in or the way they bill their customers. The classification is about statistical exposure for the bank, not about your character or competence as an operator.

Why your business might be labeled high-risk

Processors and acquiring banks weigh a handful of factors when they assess risk. In many cases it takes only one or two of these to move a business into the high-risk category.

Industry is the single biggest driver. Some sectors are flagged almost automatically because of their historical dispute and fraud rates. Beyond industry, a track record of high chargeback rates is a major red flag, since it tells the bank that your customers frequently dispute their purchases. Recurring or subscription billing adds risk because customers forget about renewals and dispute them. Large average ticket sizes increase the potential loss on any single transaction. Heavy international or cross border volume introduces fraud and compliance exposure. And operating in a tightly regulated niche means the bank inherits some of that regulatory burden.

If disputes are already a concern for your business, our companion guide on how to reduce chargebacks explains how to bring that number down before it threatens your account.

Common high-risk industries

While every processor maintains its own list, certain industries are widely treated as high-risk across the payments world. These include travel and ticketing, subscription boxes and continuity programs, nutraceuticals and supplements, CBD and hemp products, online gaming and gambling, adult content and services, firearms and accessories, debt collection and credit repair, dating services, e-cigarettes and vaping, and forex or cryptocurrency related businesses.

If your business sits in one of these categories, it does not mean you have done anything wrong. It means you should plan from the outset to work with a processor that understands your vertical, rather than a one size fits all platform that may approve you quickly and then shut you down weeks later when its risk team takes a closer look.

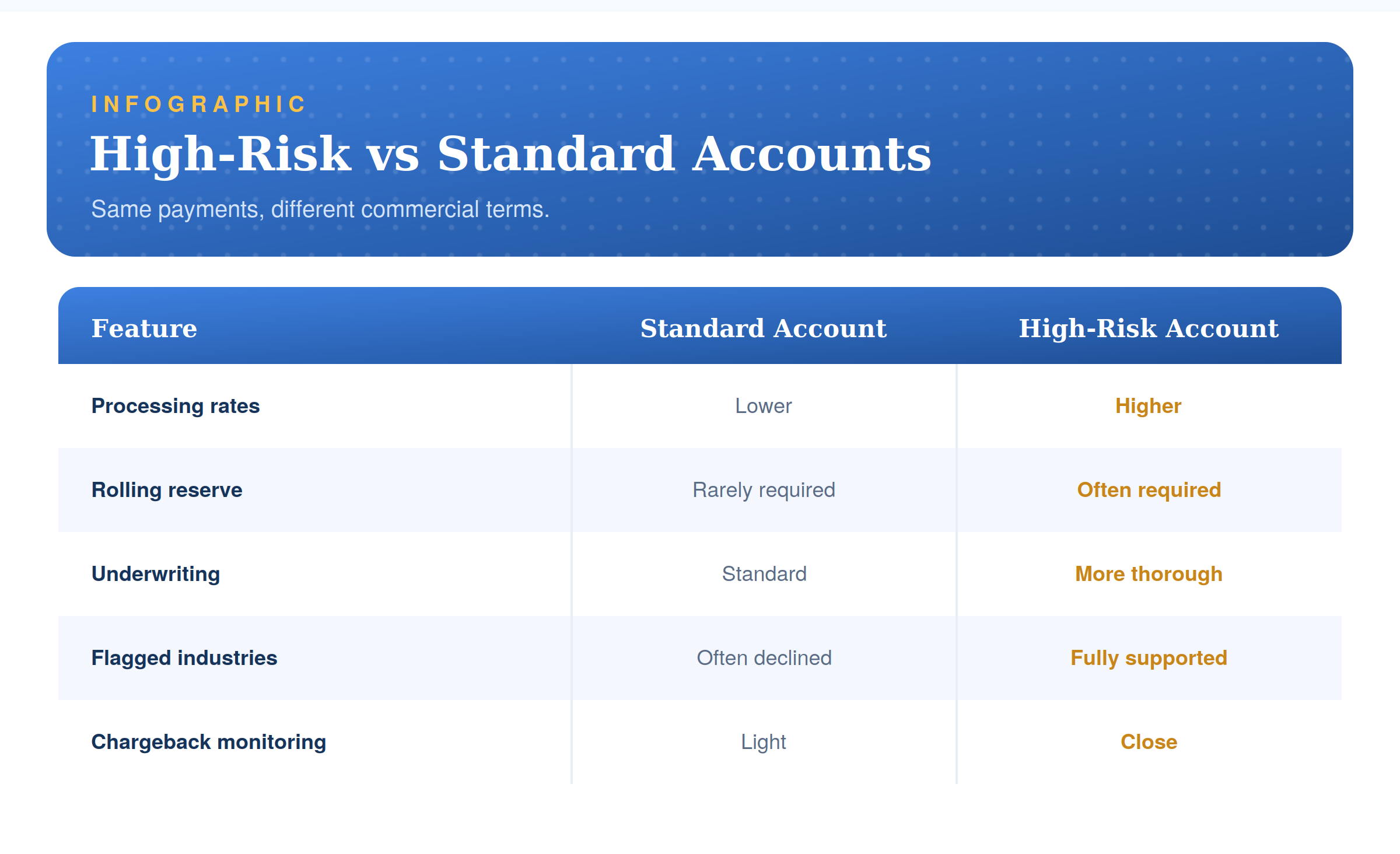

High-risk vs standard merchant accounts

The mechanics of accepting a payment are the same whether your account is standard or high-risk. The customer taps or enters a card, the transaction is authorized, and funds are settled into your account. What differs is the commercial terms that sit around that process.

As the comparison shows, high-risk accounts typically carry higher processing rates, are more likely to require a rolling reserve, and go through more thorough underwriting. In return, you receive something a standard processor often will not give a flagged business at all, which is stable, long term access to card payments without the constant threat of sudden account closure. For a refresher on the underlying flow of funds, see our overview of how payment processing works.

What to expect: pricing, reserves, and underwriting

Going in with clear expectations makes the whole experience far less stressful. Here is what high-risk processing usually involves.

Processing rates and fees

High-risk accounts generally cost more to operate than standard ones. The exact rate depends on your industry, your processing history, your average ticket size, and your monthly volume. Rather than focusing only on the headline rate, look at the full picture, including transaction fees, monthly fees, gateway fees, and any chargeback fees. A slightly higher rate from a processor that keeps your account stable is almost always cheaper than a low rate from a provider that freezes your funds.

Rolling reserves

Many high-risk accounts come with a rolling reserve, which is a percentage of your sales that the processor holds temporarily to cover potential chargebacks. A common structure is to hold around ten percent of each day's sales for roughly six months, then release those funds back to you on a rolling basis. A reserve can feel painful at first, but it is also part of what makes a processor comfortable supporting a riskier business for the long term. Understanding the reserve terms before you sign is essential for your cash flow planning.

Underwriting and documentation

Underwriting for a high-risk account is more involved than for a standard one. Expect the processor to ask for business records, several months of processing history if you have it, recent bank statements, ownership details, and sometimes a look at your website and refund policies. Preparing this documentation in advance is one of the most effective things you can do to speed up approval, because it lets the underwriting team assess your business quickly and accurately.

Contract terms

Read the agreement closely. Pay attention to the length of the contract, any early termination fees, the reserve terms, and the conditions under which the processor can adjust your rates or hold your funds. A trustworthy high-risk processor will be transparent about all of these points rather than burying them in fine print.

How to choose a high-risk payment processor

The processor you choose matters more in the high-risk world than almost anywhere else in business. Look for a provider with genuine experience in your specific industry, since that experience shapes how they price and manage your account. Confirm that they offer the gateway integrations and payment methods your customers expect. Ask about their fraud and chargeback tools, because strong payment security protections directly affect your dispute rates. Check whether they support multiple acquiring banks, which adds resilience if one bank changes its appetite for your vertical. Finally, weigh the quality of their support, because when something goes wrong with payments, slow help is expensive help.

How to get approved

Approval is very achievable when you approach it methodically. Start by getting your documentation in order, since clean records make underwriting smoother and faster. Choose a processor that specializes in your industry rather than a generic platform, because a specialist is far less likely to reverse course after approval. Be honest and complete in your application, as underwriters value transparency and tend to penalize surprises. Once the processor has reviewed your business and offered terms, you will integrate your gateway, configure your merchant accounts, and add fraud and chargeback tools. After you go live, monitor your approval rates, dispute ratios, and reserves closely so you can catch problems early.

With complete documentation, this process often takes anywhere from one to two weeks, depending on your industry and processing volume.

How to keep your account healthy

Getting approved is only half the work. Keeping your account in good standing is what protects your business over the long term. Keep your chargeback ratio low by preventing disputes before they happen. Use the fraud screening tools your processor provides, including address and card verification and 3-D Secure where appropriate. Maintain a clear, recognizable billing descriptor so customers do not mistake your charges for fraud. Respond promptly to any disputes that do arise, and keep proof of delivery and customer communication on file. Modern fraud defense increasingly relies on machine learning, which you can read about in our piece on how AI detects payment fraud.

Common mistakes to avoid

A few avoidable mistakes account for most of the trouble high-risk merchants run into. The first is hiding the true nature of the business during underwriting, which almost always backfires when the processor discovers it later. The second is choosing a generic, low cost processor that is not built for risk, then losing the account without warning. The third is ignoring the chargeback ratio until it crosses a network threshold and triggers a monitoring program. The fourth is failing to read the reserve and contract terms, which leads to cash flow surprises. Avoiding these four traps puts you ahead of most businesses in your category.

Free Demo with Chris

Free Demo with Chris

.webp)