TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

The way businesses get paid is changing faster than ever. Customers now expect checkout to be instant, invisible, and secure. The tools to deliver that experience are finally maturing at scale. What used to be a competitive edge is quickly becoming table stakes: if paying you is slower or clunkier than paying the business next door, you lose the sale before the cart is even full.

This guide breaks down the 2026 payment trends worth your attention, why each one is gaining momentum, and the practical steps you can take to stay ahead instead of scrambling to catch up. Whether you run a single storefront, a growing e-commerce brand, or a multi-location operation, the shifts below will touch how you accept money, how much it costs you, and how well you hold on to revenue.

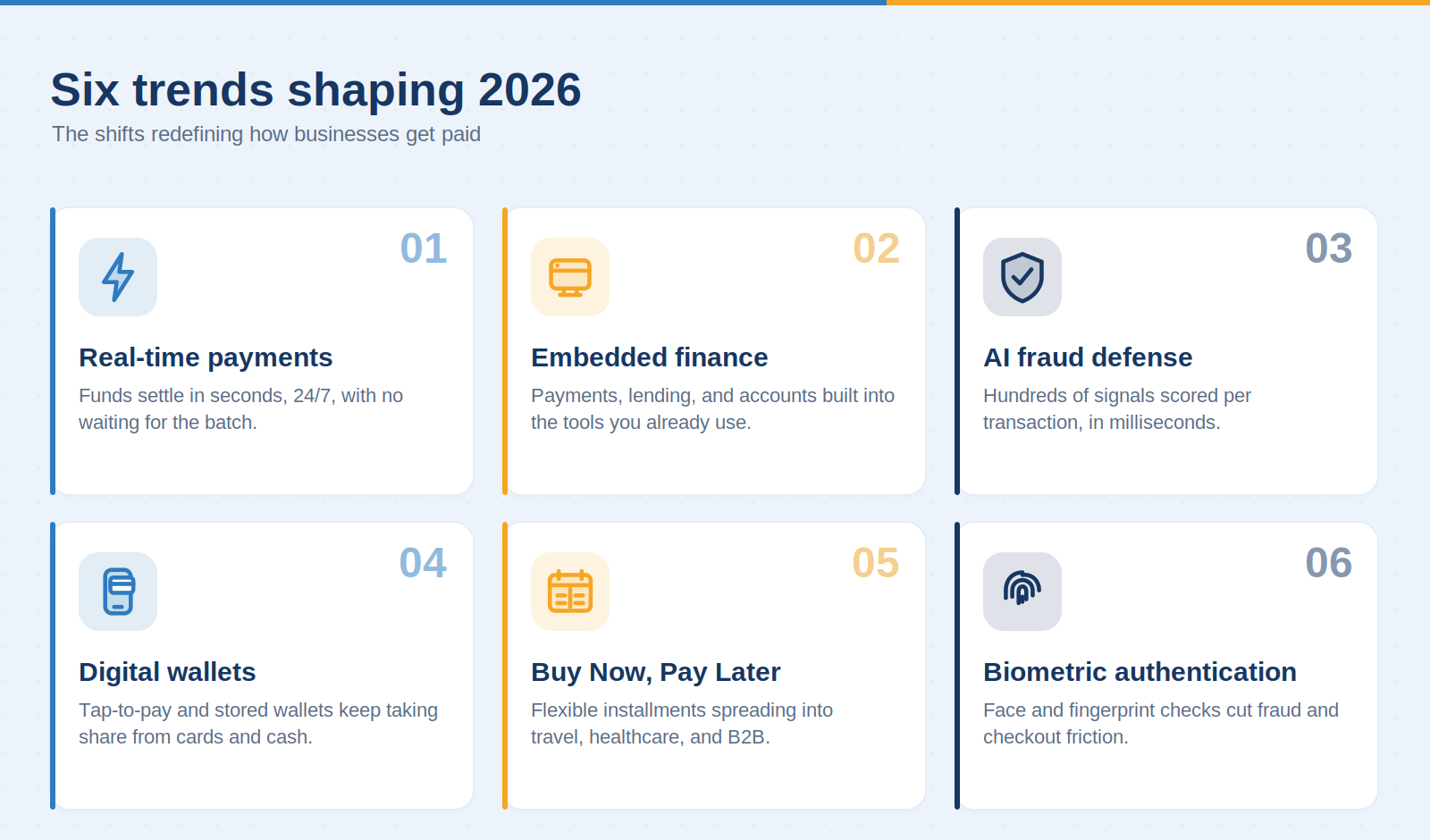

The six trends shaping 2026

1. Real-time payments become the default expectation

For years, "the money's on its way" meant waiting one to three business days while funds crawled through batch processing. That delay is disappearing. Instant account-to-account rails now settle funds in seconds, around the clock, weekends and holidays included, improving cash flow for businesses and instant gratification for customers.

In the U.S., infrastructure like the Federal Reserve's FedNow Service and the private-sector RTP network have moved real-time settlement from pilot to production. For merchants, faster access to cash means less reliance on short-term financing, smoother payroll, and the ability to pay suppliers exactly when it makes sense, not whenever the batch clears. Expect 2026 to be the year customers simply assume their payment lands the moment they hit "send."

2. Embedded finance blurs the line between software and banking

Embedded finance continues to dissolve the boundary between the software businesses use and the financial services they need. Payments, lending, insurance, and even full bank accounts are being built directly into the platforms companies already run on, so a contractor invoices and gets paid inside their job-management app, and a retailer accesses a working-capital advance without ever visiting a bank.

For business owners, the appeal is fewer logins, fewer reconciliations, and fewer vendors to manage. The trend is also reshaping expectations around the payment gateway itself: instead of a separate checkout bolted onto a website, payments increasingly live natively wherever the transaction happens. If your tools don't talk to each other yet, 2026 is the year to close those gaps.

3. AI fraud defense moves from premium add-on to baseline requirement

Artificial intelligence has shifted from a "nice to have" anti-fraud upgrade to a non-negotiable layer of protection. Modern systems analyze hundreds of signals per transaction (device fingerprints, behavioral patterns, velocity, geolocation) in milliseconds, catching fraud that static rules miss while letting legitimate customers through without friction.

The stakes are rising alongside the technology: the same generative tools that help businesses also help bad actors craft convincing synthetic identities and social-engineering attacks. Strong fraud screening protects both your revenue and your chargeback ratio, which in turn protects your processing relationships. For a deeper look at how this works under the hood, see our guide on how AI detects payment fraud.

4. Digital wallets keep eating cards and cash

Tap-to-pay and stored digital wallets (Apple Pay, Google Pay, and a growing list of regional players) keep gaining share at the expense of both physical card swipes and cash. Wallets are fast, they live on a device customers never put down, and they layer in tokenization and biometric confirmation by default, which makes them more secure than a card number typed into a form.

For merchants, the practical takeaway is simple: if your checkout doesn't accept the wallets your customers already use, you're adding friction at the exact moment they're ready to buy. Supporting contactless payments in-store and one-tap wallets online is among the highest-return changes you can make to conversion. Note that many wallet transactions still run on card rails behind the scenes, so wallets complement, rather than fully replace, your existing card acceptance.

5. Buy Now, Pay Later expands into new verticals

Buy Now, Pay Later (BNPL) financing has graduated from fashion and electronics into travel, healthcare, home services, and B2B purchasing. Customers increasingly expect a flexible, interest-transparent way to split a purchase at checkout, and offering it can lift both conversion rates and average order value.

The trade-off is added complexity and shifting oversight. The U.S. Consumer Financial Protection Bureau has signaled closer scrutiny of BNPL providers, and merchants should choose partners carefully and keep refund and dispute handling tight. Done well, BNPL removes a price objection without putting credit risk on your books. Done carelessly, it complicates reconciliation and customer service.

6. Biometric authentication streamlines secure checkout

Face and fingerprint verification are quietly becoming the most pleasant security upgrade customers have ever experienced, because it removes work rather than adding it. Instead of remembering a password or fishing a one-time code out of a text message, the customer simply looks at their phone or touches a sensor.

Backed by standards from bodies like the FIDO Alliance, biometrics reduce account-takeover fraud and cart abandonment at the same time. As passkeys and on-device authentication spread, expect biometric confirmation to become a standard part of the checkout flow rather than a novelty, especially for higher-value or recurring transactions.

What's driving the change

Three forces sit underneath all six trends, and understanding them helps you anticipate what comes next rather than just reacting to it.

Consumer expectations set by the best apps have made friction unacceptable. When the easiest checkout someone has ever used becomes their baseline, every slower experience feels broken by comparison, and abandoned carts are the result.

Faster, modernized infrastructure has made instant settlement and richer data feasible at scale. Ongoing payments-system modernization tracked by the U.S. Federal Reserve, combined with the spread of real-time rails, means capabilities that were once enterprise-only are now within reach of small businesses.

Rising and more sophisticated fraud has pushed security and authentication to the center of the checkout experience. As attacks get smarter, the defenses (tokenization, AI screening, biometrics) have to be smarter too, and they increasingly need to work without slowing legitimate customers down.

What this means for small and mid-sized businesses

It's easy to read a trends list and assume it's written for enterprises with dedicated payments teams. It isn't. The most consequential shift of 2026 is that these capabilities have become accessible to businesses of every size, usually through the processor or platform you already work with, rather than a six-figure integration project.

The risk for smaller operators isn't being unable to adopt these tools; it's adopting them piecemeal, ending up with a tangle of disconnected systems, mismatched fees, and security gaps. The businesses that win will be the ones that treat their payment stack as a connected system, where acceptance, fraud protection, settlement, and reporting all work together, instead of a pile of one-off add-ons. If your industry carries elevated risk, that planning matters even more; start with our guide to high-risk merchant accounts.

How to future-proof your payments

Trends only matter if you act on them. Here's a practical sequence to stay competitive without overhauling everything at once.

1. Audit your stack. Begin by mapping every payment method, fee, and integration you currently rely on. You can't optimize what you can't see, and most businesses discover overlapping tools and processing fees they didn't know they were paying.

2. Offer the right methods. Add the wallets, local payment methods, and financing options your customers actually expect at checkout. The goal isn't to accept everything. It's to remove every reason a ready buyer might hesitate.

3. Strengthen security. Layer in tokenization, AI-driven fraud screening, and PCI DSS compliance as a baseline, not an afterthought. Strong security protects revenue, reputation, and your standing with processors all at once.

4. Automate and integrate. Connect payments to your billing, accounting, and reconciliation systems to cut manual work and reduce errors. Every hour spent matching transactions by hand is an hour not spent growing.

5. Review and optimize. Revisit approval rates, decline reasons, and total costs on a regular cadence as you grow. Payments isn't a set-and-forget decision. Small, steady improvements compound into meaningful margin.

Free Demo with Chris

Free Demo with Chris

.webp)