TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

If your business runs on recurring invoices, B2B payments, large transactions, or subscription billing, you've probably felt the sting of credit card fees eating into your margins. That's why more and more businesses are adding ACH payment processing to their checkout. It's cheaper, more stable, and surprisingly flexible.

In this guide, we'll walk through what ACH is, how it works, where it shines, and how to get started.

What Is ACH Payment Processing?

ACH stands for Automated Clearing House, a U.S. electronic payment network governed by Nacha that moves funds between bank accounts. Instead of running a card, an ACH payment pulls money directly from a customer's checking or savings account and deposits it into yours.

You may also hear ACH referred to as:

- Electronic check (eCheck) processing

- Bank transfers or bank debits

- Direct debit

- EFT (electronic funds transfer)

While they have slight technical differences, in practice they all describe the same general process: moving money bank-to-bank, no card required.

How an ACH Transaction Works

Behind the scenes, an ACH payment moves through a few clear steps:

- Authorization. The customer authorizes the payment by entering their routing and account numbers, signing a form, or agreeing to recurring terms.

- Submission. Your ACH processor or payment provider batches the transaction and submits it to the ACH network.

- Clearing. The ACH network routes the transaction to the customer's bank (the Receiving Depository Financial Institution, or RDFI).

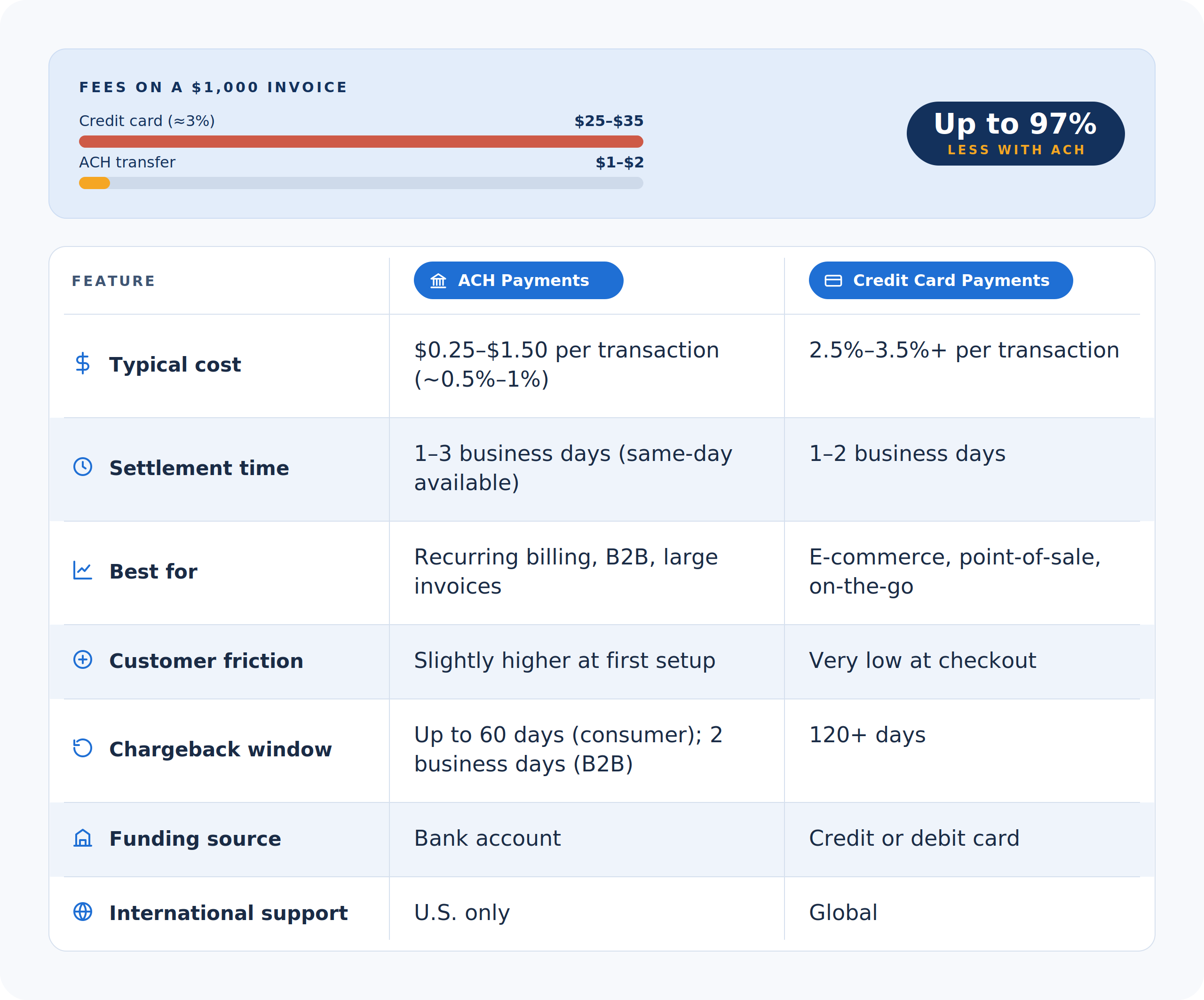

- Settlement. The funds are debited from the customer's account and credited to your business account, typically in one to three business days. Same-day ACH is also available for many transactions.

The result: a low-fee, predictable payment method that's especially useful for recurring and high-value transactions.

ACH vs Credit Card Processing: Which Should You Use?

ACH and credit card payments aren't competitors so much as complements. Most modern businesses offer both. Here's how they stack up.

If you're running a SaaS company, a property management business, a B2B distributor, a healthcare practice, or any business with regular large invoices, ACH typically delivers dramatic savings versus card processing.

Best Use Cases for ACH Payment Processing

Some of the strongest use cases include:

- Subscription and SaaS billing. Lower processing costs preserve margin on every renewal.

- B2B payments. Large invoices that would carry expensive interchange fees on cards become affordable via ACH.

- Real estate, rent, and HOA dues. Predictable, recurring monthly payments.

- Insurance premiums. Customers prefer not to put policy payments on credit cards.

- Healthcare and dental. Patient payment plans and recurring billing.

- Nonprofits and memberships. Recurring donations and dues without donor fatigue from card declines.

- Professional services. Law, accounting, consulting, and agency retainers.

In each of these cases, the customer relationship is ongoing, the amounts are meaningful, and the savings compound quickly.

Benefits of Adding ACH to Your Payment Stack

1. Significantly lower fees

The single biggest benefit. On a $1,000 invoice, ACH might cost you a dollar or two. The same invoice on a credit card could cost $25 to $35 in processing fees. Over hundreds or thousands of transactions, the savings are enormous.

2. Fewer declines on recurring billing

Cards expire, get lost, get reissued, and get declined. Bank accounts change far less often, so ACH-based recurring billing typically has higher success rates on renewal cycles.

3. Better for high-ticket transactions

Some processors cap card transaction amounts or apply extra scrutiny to large charges. ACH is well-suited for transactions in the thousands or tens of thousands of dollars.

4. Strong customer preference for B2B

Most business buyers expect to pay invoices by ACH, wire, or check. Offering ACH meets them where they already are.

5. Predictable cash flow

Once ACH is set up, recurring payments draft automatically. That reliability translates to easier forecasting and fewer collections headaches.

What Are the Risks and Limitations?

ACH isn't without trade-offs. The main considerations:

- Settlement is slower. Standard ACH funds in one to three business days. Same-day ACH is available but carries higher fees and per-transaction caps.

- Returns and reversals. A customer can return an ACH transaction for reasons like insufficient funds, unauthorized debit, or stop payment. Return fees apply, so monitor your return rate closely.

- U.S.-only. ACH does not support international bank accounts. International equivalents (SEPA in Europe, for example) operate on different networks.

- Setup friction. Customers must provide their routing and account numbers, which can be a slight conversion hurdle compared to a card form.

- Compliance requirements. You must obtain proper authorization (Nacha rules are strict) and securely store bank account data.

The right processor manages most of these risks for you with verification tools, return monitoring, and Nacha-compliant authorization flows.

How to Get Started with ACH Payment Processing

Here's a straightforward roadmap to add ACH to your business:

- Choose a processor that offers both ACH and card processing. Having one provider for both keeps reconciliation simple.

- Apply and underwrite. ACH approval involves reviewing your business, expected volume, average ticket, and return history.

- Integrate with your gateway, billing system, or invoicing tool. Most modern platforms support ACH via APIs or built-in integrations.

- Set up authorization flows. Make sure your checkout, intake forms, or invoices include compliant ACH authorization language.

- Use account verification tools. Tools like instant bank verification reduce returns from typos and closed accounts.

- Offer ACH at the right moments. Highlight it for B2B customers, large invoices, and renewals where it benefits both sides.

What to Look for in an ACH Provider

Not every payment processor offers strong ACH capabilities. When evaluating providers, prioritize:

- Transparent flat or capped per-transaction pricing

- Same-day ACH availability for time-sensitive payments

- Account verification and fraud screening tools

- Recurring billing and customer vault

- Robust reporting and return management

- A unified platform that handles ACH, credit card, and international payments together

- Responsive support that can help with returns, disputes, and compliance questions

How TCB Pay Powers ACH for Businesses

At TCB Pay, ACH payment processing is a core part of our platform. Our customers use ACH to:

- Bill subscription and SaaS customers at a fraction of card processing costs

- Collect rent, dues, and recurring invoices automatically

- Accept large B2B payments without sacrificing margin

- Power high-volume payouts and disbursements

- Reduce failed renewals and improve customer retention

Everything runs through one secure gateway with built-in tools for verification, recurring billing, returns monitoring, and Nacha-compliant authorization. You get the savings of ACH, the convenience of card, and one provider to support both.

Free Demo with Chris

Free Demo with Chris

.webp)