Interchange fees are a cornerstone of the payments ecosystem, yet they often remain poorly understood by businesses and consumers alike. These fees, applied to every card-based transaction, significantly influence the cost of payment processing. Determined and regularly updated by major card networks like Mastercard and Visa, interchange fees reflect the complexity of maintaining secure and efficient payment systems. Let’s explore what interchange fees are, how they work, and strategies to manage them effectively.

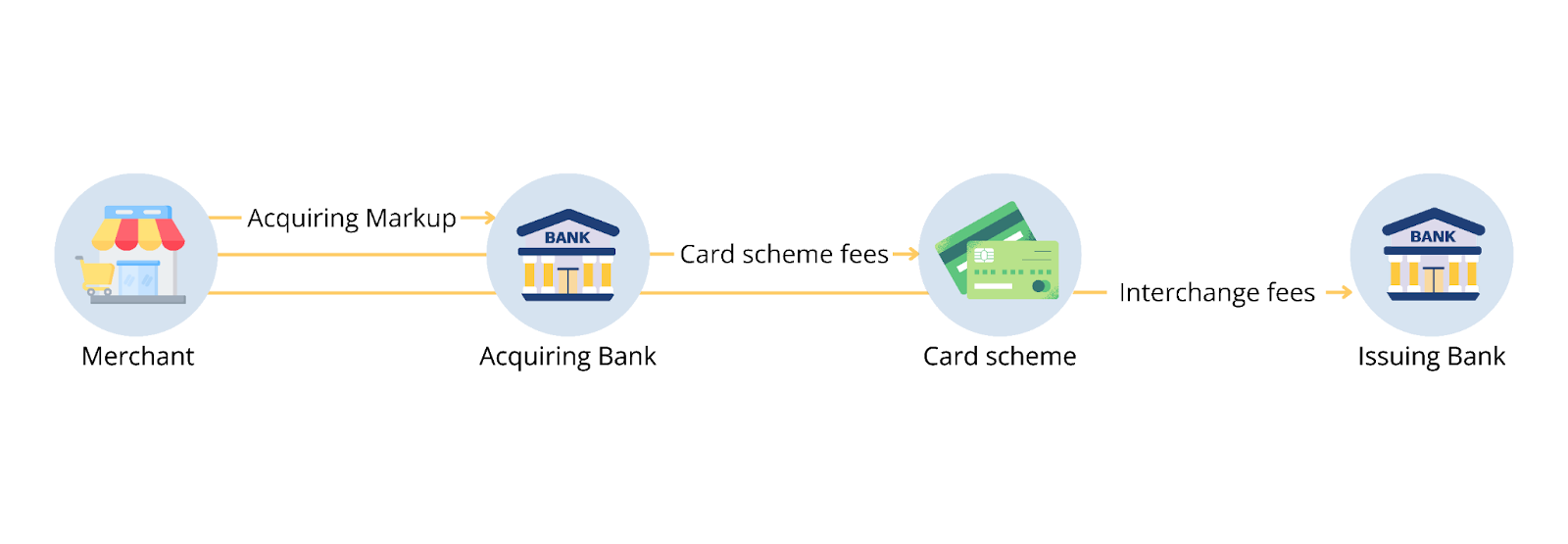

Interchange fees are transaction fees that a merchant’s bank (the acquiring bank) pays to the cardholder’s bank (the issuing bank) whenever a customer makes a purchase using a credit or debit card. These fees are intended to cover the risks and costs associated with card transactions, such as fraud prevention, customer service, and technology maintenance.

For instance, when a customer uses a credit card to pay for a product, the issuing bank ensures that the merchant receives payment while bearing the risk of the cardholder not repaying their credit balance. Interchange fees compensate the issuing bank for this risk and the infrastructure required to facilitate these transactions.

Interchange fees are typically calculated as a percentage of the transaction amount, plus a fixed fee. For example, a fee structure might be 2.5% + $0.10 per transaction. The exact rates depend on several factors, including:

Card Type: Premium credit cards with higher rewards often carry higher interchange fees compared to standard cards.

Transaction Method: Transactions where the card is physically present (e.g., in-store purchases) generally have lower interchange fees compared to card-not-present transactions (e.g., online purchases) due to differing fraud risks.

Merchant Category Code (MCC): Certain industries, such as grocery stores or charities, may qualify for lower interchange rates.

According to the Federal Reserve, the average interchange fee for debit card transactions in the United States was $0.23 per transaction in 2022. This represents approximately 0.65% of the average transaction value. For regulated debit cards, the average fee was capped at $0.22 plus 0.05% of the transaction amount, in accordance with the Durbin Amendment. In contrast, fees for unregulated debit cards averaged 1.15% of the transaction value.

Interchange fees can significantly impact a business’s bottom line, particularly for companies with high transaction volumes or low margins. Understanding these fees is essential for:

Cost Management: Knowing how much of each transaction goes toward interchange fees can help businesses identify opportunities to reduce costs.

Pricing Strategies: Businesses may incorporate interchange fees into their pricing models to maintain profitability.

While interchange fees are largely non-negotiable, businesses can take steps to optimize and potentially reduce them:

Choose the Right Payment Processor: Payment processors often bundle interchange fees with other costs. Partnering with a transparent processor can help businesses better understand and manage these expenses.

Encourage Card-Present Transactions: Transactions where the card is physically present tend to have lower interchange fees due to reduced fraud risk.

Optimize Merchant Category Codes: Ensuring that your business is classified under the correct MCC can sometimes lead to lower rates, particularly if your industry is eligible for special rates.

Implement Fraud Prevention Measures: Utilizing advanced fraud detection tools can reduce risk and lead to lower interchange fees for card-not-present transactions.

Negotiate Additional Fees: While interchange rates are set by card networks and non-negotiable, some additional processing fees can be negotiated with your payment provider.

As the payments landscape evolves, so do interchange fees. Regulatory changes, technological advancements, and shifts in consumer behavior all influence how these fees are structured and implemented. For instance, regulatory bodies in various regions have capped interchange fees to promote fairness and transparency. Additionally, the rise of alternative payment methods, such as digital wallets and real-time payments, could reshape the interchange fee landscape.

Interchange fees are an inevitable part of accepting card payments, but understanding their intricacies can empower businesses to make informed decisions. By choosing the right partners, leveraging technology, and optimizing transaction processes, businesses can better manage these costs and improve their overall profitability.

Learn more about how our transparent pricing and advanced solutions at TCB Pay can help you manage interchange fees and boost your bottom line. Explore our pricing and take the first step toward smarter payment processing today!

TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing Back to all articles

Back to all articles