TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

.webp)

If your business touches card payments in any way, PCI DSS applies to you. It sounds intimidating, but at its core the standard is just a structured way to keep cardholder data safe. This guide breaks down PCI DSS compliance in plain English: what it is, who it covers, the requirements behind it, how merchant levels and the SAQ work, and the practical steps to becoming and staying compliant.

We've written it for business owners and operators rather than security engineers, so you'll find the jargon translated as we go. Wherever something depends on your exact setup, we say so, because the single most common compliance mistake is assuming one size fits all.

What is PCI DSS?

PCI DSS (the Payment Card Industry Data Security Standard) is a set of security requirements created by the major card brands (Visa, Mastercard, American Express, Discover, and JCB) and maintained by the PCI Security Standards Council. Any organization that stores, processes, or transmits cardholder data must follow it.

It isn't a government law, but card networks and acquiring banks enforce it through their contracts. When you signed your merchant agreement, you almost certainly agreed to maintain PCI compliance. So in practice, it's mandatory, and the consequences for ignoring it are contractual and financial rather than criminal.

The standard has evolved over time. The current generation is the version 4.x family: PCI DSS v4.0 introduced a significant overhaul of the requirements, and v4.0.1 followed as a maintenance update. Older versions have been formally retired, and several v4.x requirements that were "best practice" during the transition have since become mandatory. Standards move, so always confirm the version your acquirer expects against the PCI SSC document library rather than relying on a checklist you saved a few years ago.

What counts as cardholder data?

Before you can protect card data, you have to know exactly what it is, because the rules differ sharply between two categories.

Cardholder data (CHD) includes the Primary Account Number (PAN, the long number on the front of the card), and, when stored alongside the PAN, the cardholder name, expiration date, and service code.

Sensitive authentication data (SAD) includes the full magnetic-stripe (track) data, the CAV2/CVC2/CVV2/CID security code, and PINs or PIN blocks.

The headline rule is simple: you may store certain elements of CHD if you protect them properly, but you must never store SAD after authorization, not the CVV, not the full track data, not the PIN. A surprising number of breaches come down to a system quietly logging data it was never allowed to keep. If you understand nothing else about scoping, understand that the security code on the back of the card should never live in your database, your logs, or a spreadsheet. To see where these data elements appear in a normal transaction, it helps to understand how payment processing works end to end.

Who has to comply?

Everyone who handles card data, from a corner shop with a single terminal to a global e-commerce platform. The scope and effort scale with how you accept payments and how much data you handle, but there's no "too small to comply" exemption, and "we only take a few cards a month" is not a defense after a breach.

What changes with size is how you prove it. A small merchant using a hosted, fully outsourced checkout may answer a short questionnaire and never touch raw card data, while a large processor faces an annual on-site audit. The obligation is universal; the burden is proportional.

The 6 goals of PCI DSS

The standard's 12 requirements roll up into six high-level goals. Together they cover the full lifecycle of protecting card data, from the network it travels across to the written policy that governs your team.

In short: build and maintain a secure network, protect stored and transmitted cardholder data, manage vulnerabilities with anti-malware and patching, restrict access on a need-to-know basis, monitor and test your systems regularly, and maintain a written information-security policy. For a formal definition framed for a general audience, Investopedia's overview of PCI compliance is a useful reference.

The 12 requirements at a glance

Each goal breaks down into specific requirements. You don't need to memorize them, but recognizing the shape of the list helps you spot which ones touch your business:

- Install and maintain network security controls (firewalls and the like).

- Apply secure configurations to all system components, with no vendor-default passwords or settings.

- Protect stored account data, including strong encryption and key management.

- Encrypt cardholder data whenever it crosses open, public networks.

- Protect all systems against malware and keep anti-malware current.

- Develop and maintain secure systems and software, including timely patching.

- Restrict access to cardholder data by business need-to-know.

- Identify users and authenticate access with unique IDs and strong, multi-factor authentication.

- Restrict physical access to cardholder data and the systems that hold it.

- Log and monitor all access to network resources and cardholder data.

- Test the security of systems and networks regularly, including vulnerability scans.

- Support information security with organizational policies and programs.

A useful mental model: requirements 1 to 6 keep attackers out, 7 to 9 limit who and what can reach the data, 10 to 11 make sure you'd notice if something went wrong, and 12 ties it together with policy and accountability. Pairing this with broader payment security best practices turns a compliance checklist into genuine resilience.

Merchant levels: how your size sets the rules

PCI sorts merchants into four levels based on annual transaction volume, which determines how rigorously you validate compliance. The thresholds vary slightly between card brands, but the structure is consistent.

Level 1 merchants, the largest or any merchant that has suffered a breach, face an annual on-site assessment producing a Report on Compliance (ROC), typically signed off by a Qualified Security Assessor (QSA), plus quarterly network scans by an Approved Scanning Vendor (ASV). Levels 2 through 4 generally validate with an annual Self-Assessment Questionnaire and quarterly scans, with the exact expectations set by your acquiring bank. The official thresholds live on the card brands' own sites, for example Visa's small-business security and compliance page, and your acquirer is the final word on what applies to you.

The SAQ and choosing the right one

Most small and mid-sized businesses validate using a Self-Assessment Questionnaire (SAQ), a structured set of yes/no questions confirming you meet the requirements that apply to your environment. The catch is that there are several SAQ types, and picking the wrong one is one of the most common stumbling blocks in the whole process.

Which SAQ fits depends entirely on how you accept payments:

- SAQ A: card-not-present merchants (e-commerce or mail/telephone order) who fully outsource all cardholder data handling to validated third parties; you never see or store card data.

- SAQ A-EP: e-commerce merchants who don't directly receive card data but whose website affects how the payment is captured (for example, a partially hosted or redirected checkout).

- SAQ B: merchants using only standalone, dial-out terminals or imprint machines, with no electronic storage.

- SAQ B-IP: merchants using standalone, IP-connected payment terminals, with no electronic storage.

- SAQ C-VT: merchants who key transactions into a web-based virtual terminal on an isolated computer.

- SAQ C: merchants with payment application systems connected to the internet, with no electronic storage of card data.

- SAQ P2PE: merchants using a validated point-to-point encryption solution, with no electronic storage.

- SAQ D: the catch-all for everyone who doesn't fit the categories above, including most service providers; it covers all applicable requirements.

If two types seem to fit, you've probably mis-mapped your environment, so confirm with your processor before you start, because answering the wrong SAQ can leave real gaps unaddressed.

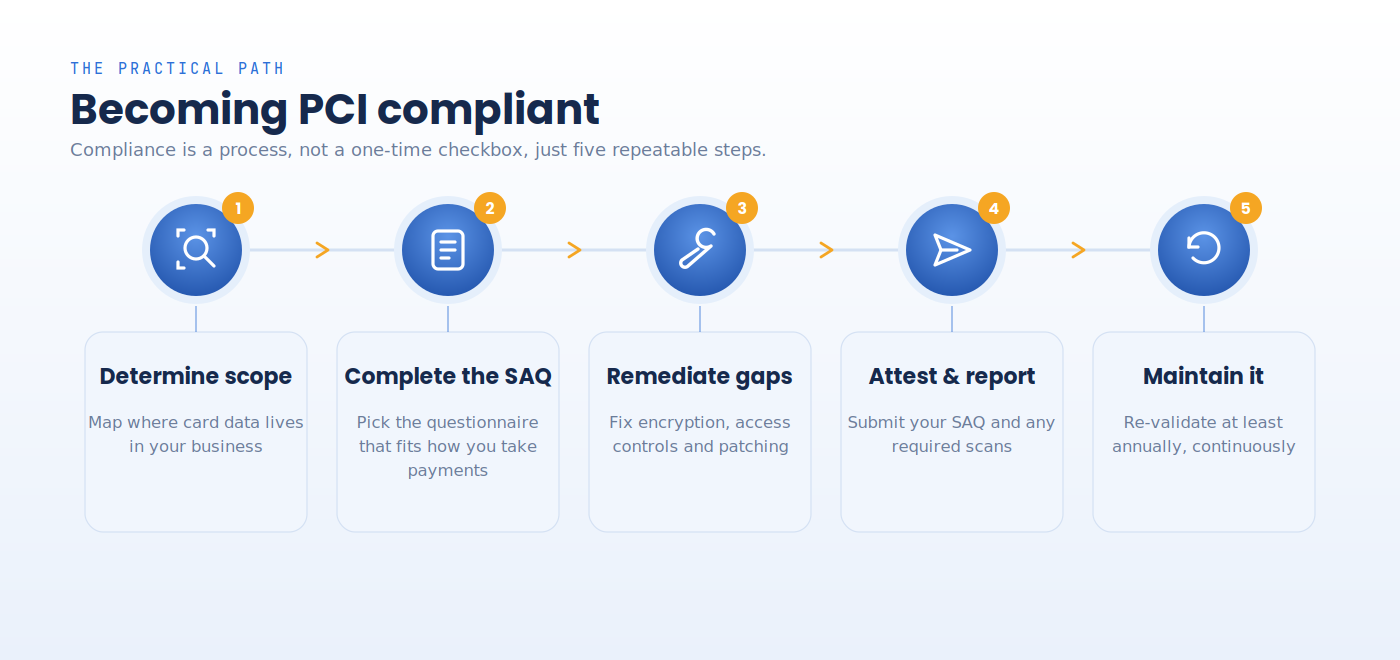

How to become compliant

Compliance is a process, not a one-time checkbox. Here's the practical path, and what each step actually involves.

1. Determine your scope. Map every place card data is captured, processed, transmitted, or stored, including the systems connected to those places. This is the step people rush and regret. Anything "in scope" must meet the requirements, so an accurate map is also your best tool for shrinking the work.

2. Complete the right SAQ. Using the scope you mapped, confirm the SAQ type that matches how you take payments, then work through it honestly. A "no" answer isn't a failure; it's a to-do item.

3. Remediate any gaps. Close what the SAQ surfaced: turning on encryption, tightening access controls, enforcing multi-factor authentication, patching, and removing any prohibited stored data. Fix the riskiest gaps first.

4. Attest and report. Submit your completed SAQ and Attestation of Compliance, along with any required ASV scan results, to your acquirer or as your processor directs.

5. Maintain it continuously. Compliance is validated at least annually, but the controls must hold every day in between. Scans run on a schedule, staff change, software updates roll out: treat it as an ongoing program, not an annual scramble.

How to shrink your PCI scope

The single most effective compliance strategy is to handle less card data, ideally none in your own systems. The less cardholder data touches your environment, the fewer requirements apply and the simpler your SAQ becomes. A few proven approaches:

- Tokenization replaces the real card number with a meaningless token, so your systems store something that's worthless to a thief.

- Point-to-point encryption (P2PE) encrypts card data at the point of capture so it's never readable inside your environment.

- Hosted fields and redirects keep the actual card entry on your provider's validated infrastructure, not your page.

Used together, these can move many e-commerce merchants toward the shortest SAQ. This is exactly where working with a compliant, well-integrated processor pays off: it does the heavy lifting and keeps your environment out of the riskiest parts of the data flow.

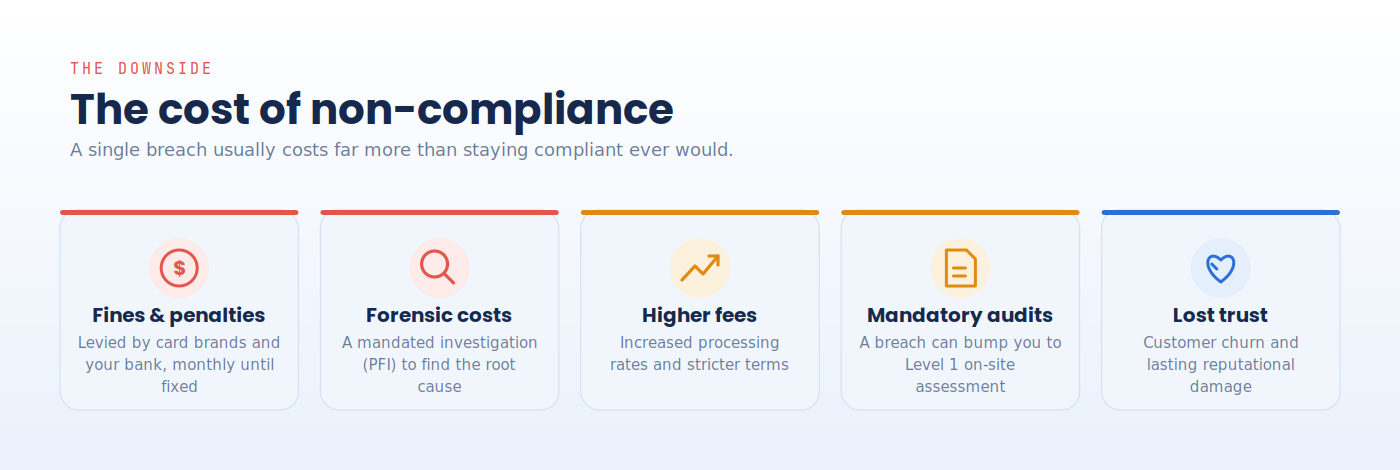

The cost of non-compliance

Falling out of compliance is expensive, and the bill almost always dwarfs the cost of doing the work up front.

A breach can trigger fines from the card brands and your bank (often charged monthly until you remediate), a mandatory forensic investigation, higher processing fees, and a forced bump to stricter validation. On top of the direct costs sits the hardest one to recover from: lost customer trust. Industry research consistently puts the average cost of a data breach in the millions; the long-running IBM Cost of a Data Breach report is a sobering annual benchmark. Demonstrated compliance at the time of an incident can reduce some penalties, which is one more reason to keep your documentation current.

Common mistakes to avoid

A handful of missteps account for a large share of compliance trouble:

- Storing what you shouldn't. Logging the CVV or full track data "just in case" is both a violation and a liability. Don't.

- Choosing the wrong SAQ. It quietly narrows the questions you answer and can hide real gaps.

- Underscoping. Forgetting connected systems, back-office tools, or that one legacy server keeps card data flowing through unprotected places.

- Treating it as annual. Compliance lapses the moment a control slips, not on your renewal date.

- Assuming the processor covers everything. Outsourcing shrinks your scope dramatically but never eliminates your own responsibilities.

Free Demo with Chris

Free Demo with Chris.webp)

.webp)