TCB Pay Portal

TCB Pay Portal TCB Pay App

TCB Pay App ACH

Processing

ACH

Processing TCB Pay Issuing

TCB Pay Issuing Alert & Notifications

Alert & Notifications TCB Pay White-Label

TCB Pay White-Label Integrations

Integrations IT Solutions

IT Solutions About

Us

About

Us Pricing

Pricing Blog

Blog Security

Security System Status

System Status Contact Us

Contact Us Sign in to TCB Pay Issuing

Sign in to TCB Pay Issuing

Back to all articles

Back to all articles

.webp)

Most payment issues don’t start with fraud, chargebacks, or compliance failures.

They start with invisible signals businesses don’t know are being tracked.

In 2026, banks, card networks, and processors continuously evaluate merchants long before any restriction, reserve, or shutdown occurs. These evaluations are not based on intuition or isolated incidents. They are driven by behavioral patterns, stability metrics, and operational consistency that most businesses never see and rarely monitor.

That gap between what you track and what financial institutions assess is where risk quietly builds.

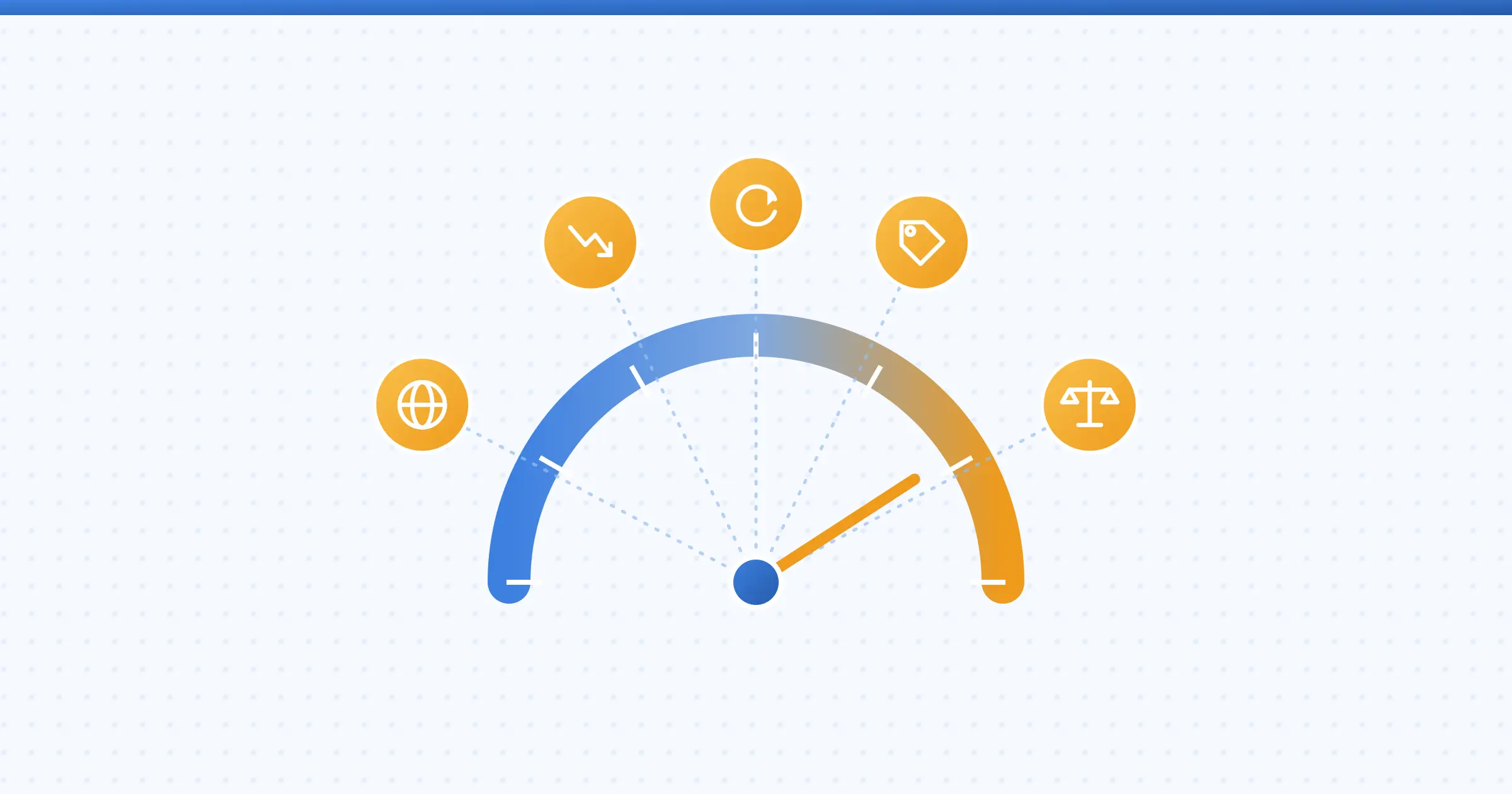

What Banks, Card Networks, and Processors Actually Monitor in 2026

Most businesses believe payment risk shows up suddenly.

An account freeze. A reserve. A shutdown.

In reality, payment risk builds quietly.

Long before a restriction happens, banks and card networks are already evaluating your activity. They are watching patterns, stability, and behavior that most merchants never see and rarely track.

In 2026, the biggest risk is not fraud itself.

It is operating without knowing how your payments look from the outside.

This article breaks down what financial institutions actually monitor and the checklist most growing businesses fail without realizing it.

What Your Bank Sees That You Don’t

From your dashboard, payments look simple. Transactions are approved, settlements arrive, revenue grows.

From the bank’s side, the picture is very different.

They see velocity changes across short periods, not just monthly growth.

They see how transaction timing clusters, especially during promotions or campaigns.

They monitor refund behavior, including how fast refunds are issued and how often they follow disputes.

They analyze descriptor consistency and customer recognition signals.

They track cross border activity spikes and geographic shifts.

None of these signals alone are a problem.

Together, they tell a story.

And that story determines whether your account is considered stable or risky.

The Metrics That Trigger Reviews Before a Shutdown

Most merchants focus on chargeback ratios because they are visible and well known. By the time chargebacks spike, it is already late.

In 2026, reviews are triggered earlier by patterns such as:

- Approval volatility across short timeframes

- Sudden changes in average order value

- Refund volume increasing faster than revenue

- Settlement inconsistencies between processing channels

- Transaction velocity outpacing historical norms

- Mismatches between issuing, processing, and payout data

Two businesses with the same revenue can receive completely different risk outcomes based on these signals alone.

Why “Good Months” Can Still Flag Your Account

Growth without structure looks like risk.

A strong sales month can trigger monitoring if it comes with unstable transaction behavior or incomplete reporting. Fast growth that is not supported by consistent controls raises more questions than slow, predictable scaling.

This is why some businesses are surprised when issues appear during their best performing periods.

From the bank’s perspective, instability matters more than volume.

Being Compliant Is Not the Same as Being Monitorable

Many merchants are technically compliant.

They have the right documents, policies, and approvals.

But compliance alone is no longer enough.

Banks expect businesses to be monitorable. That means having clear, real time visibility into activity, controls that scale with volume, and the ability to explain changes quickly.

When data is fragmented across processors, issuing platforms, and payout tools, even healthy businesses struggle to answer basic questions during reviews.

The Payment Risk Checklist Most Businesses Don’t Track

If you are not tracking these weekly, you are operating blind:

- Transaction velocity trends

- Approval rate stability, not just averages

- Refund timing relative to disputes

- Average order value consistency

- Settlement timing and reconciliation gaps

- Cross border transaction shifts

- Descriptor consistency across channels

- Dispute reason code patterns

This checklist is what financial institutions expect you to understand, even if they never explicitly ask for it.

Why Infrastructure Determines Risk Outcomes

Payment risk in 2026 is operational.

Disconnected tools create blind spots. Blind spots create delays. Delays turn manageable issues into account level problems.

This is why modern payment infrastructure is built around unified visibility, real time data, and integrated controls rather than isolated tools.

TCB Pay supports businesses by centralizing processing, issuing, monitoring, and reporting so risk signals are visible early and manageable before they escalate.

If you do not know how your payment activity looks from the outside, you are relying on luck.

In 2026, payment stability is not about avoiding problems.

It is about seeing them early enough to stay in control.

Free Demo with Chris

Free Demo with Chris